Week of April 29, 2024 in Review

The Fed once again held rates steady, labor sector data showed signs of softening, and there’s more evidence of rising home values across the country. Read on for these stories and more:

- Fed Shuts Down Rate Hike Chatter

- Jobs Report Shows Softening

- Private Payrolls Beat Estimates

- Job Openings Hit 3-Year Low

- Trends in Unemployment Persist

- Home Price Gains Continue

Fed Shuts Down Rate Hike Chatter

After eleven rate hikes since March 2022, the Fed once again left their benchmark Federal Funds Rate unchanged at a range of 5.25% to 5.5%. This decision was unanimous and marks the sixth straight meeting they held rates steady.

The Fed Funds Rate is the interest rate for overnight borrowing for banks and it is not the same as mortgage rates. The Fed has been aggressively hiking the Fed Funds Rate throughout this cycle to try to slow the economy and curb the runaway inflation that became rampant over the last few years.

What’s the bottom line? After some recent inflation readings were hotter than expected, some economists wondered if the Fed would resume hikes to the Fed Funds Rate. However, Fed Chair Jerome Powell emphasized a hike was “unlikely,” adding that the Fed would instead keep the Fed Funds Rate at its current level if tighter conditions were warranted.

Powell also reiterated that the Fed does not expect to cut rates until members are confident that inflation is moving sustainably towards their 2% target as measured by annual Core Personal Consumption Expenditures, which is at 2.8% as of March.

However, a sharp rise in the unemployment rate (which has been in a narrow range between 3.7% and 3.9% since August) could also impact the timing for rate cuts. While the Fed’s latest forecasts showed that seventeen of nineteen Fed members don’t see the unemployment rate rising above 4.1%, an increase over this level could pressure the Fed to cut rates, given their dual mandate of price stability and maximum

employment.

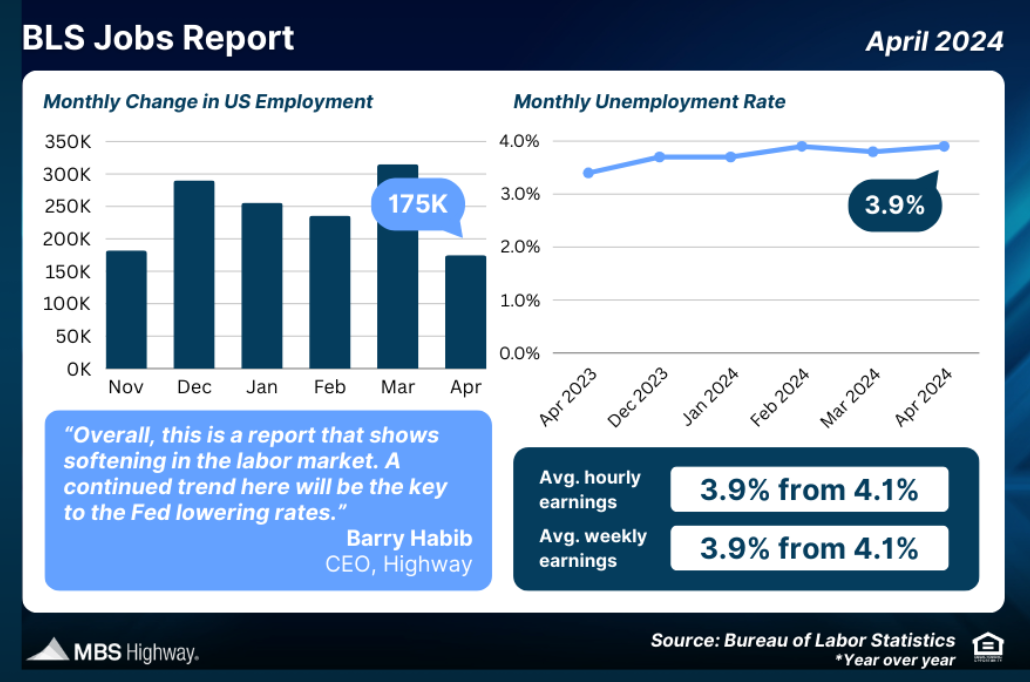

Jobs Report Shows Softening

The Bureau of Labor Statistics (BLS) reported that there were 175,000 jobs created in April, which was well below estimates of 243,000 new jobs. Revisions to February and March shaved 22,000 jobs from those months combined. The unemployment rate rose from 3.8% to 3.9%.

What’s the bottom line? The headline job number comes from the report’s Business Survey, which is based predominantly on modeling and estimations. In fact, one of the biggest reasons we saw job gains last month was the birth/death model, where the BLS estimates new business creation relative to closed businesses and how many jobs this created. In April, this modeling added 363,000 jobs to the headline figure, which would have shown a loss of 188,000 jobs otherwise.

Average weekly hours also declined slightly, which is important because one of the ways businesses cut costs is to cut the number of hours worked. This caused average weekly earnings, which is a good reflection of take-home pay, to fall 0.1% from March. Overall, the data suggests softening in the labor sector. Again, this could pressure the Fed to cut rates sooner if this trend continues.

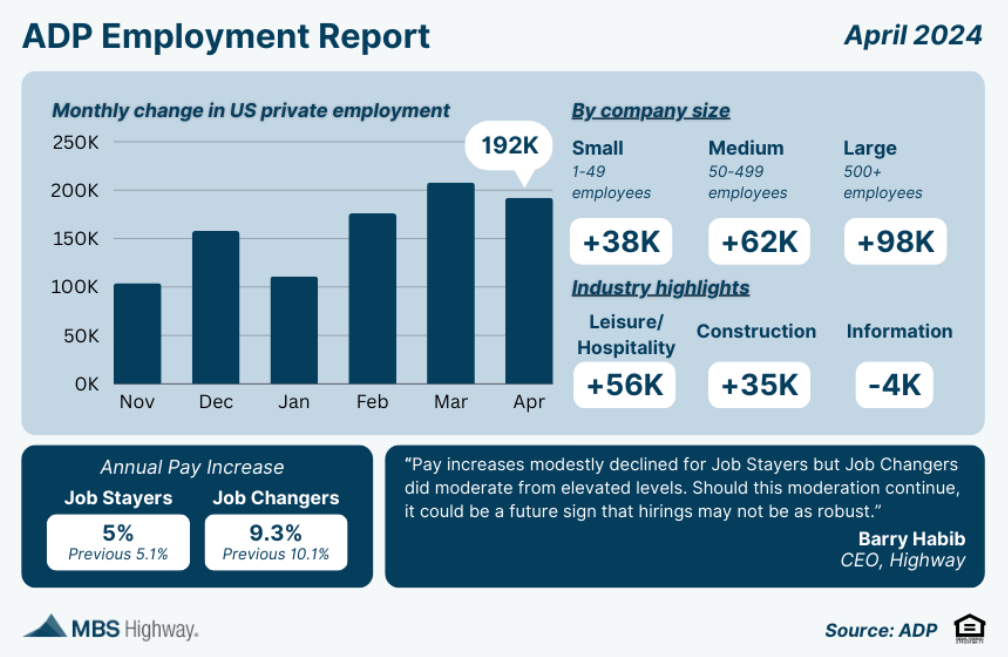

Private Payrolls Beat Estimates

ADP’s Employment Report showed that private payrolls rose more than expected in April, led by another boost from the leisure and hospitality sector. Employers added 192,000 new jobs versus the 175,000 that had been forecasted, while job growth in February was also revised higher by 24,000 jobs.

What’s the bottom line? ADP’s Chief Economist, Nela Richardson, noted that “hiring was broad-based in April” with only the information sector posting losses. Growth among small businesses remained muted, however, as businesses with fewer than 50 employees added 38,000 jobs, versus 160,000 new jobs added among medium and large companies combined.

Annual pay gains for job stayers have been decelerating, with ADP reporting an average increase of 5% in April versus 5.1% in March. Job changers saw an average increase of 9.3% and while this was a decline from 10.1% in March, it’s above the levels seen at the start of the year.

Job Openings Hit 3-Year Low

The latest Job Openings and Labor Turnover Survey (JOLTS) showed that job openings contracted to 8.488 million in March, down from 8.813 million in February and well below estimates. The hiring rate fell from 3.7% to 3.5%, while the quit rate fell from 2.2% to 2.1%.

What’s the bottom line? Job openings have reached their lowest level since March 2021, and are now well below the high of 12 million hit in 2022, suggesting some softness in the labor sector. Plus, the quit rate is at the lowest level since 2018 other than COVID. This also shows some labor sector weakness, as a lower quit rate suggests less poaching from other companies and fewer people feeling confident about finding new employment.

Trends in Unemployment Persist

Initial Jobless Claims were flat in the latest week, as 208,000 people filed for unemployment benefits for the first time. Continuing Claims also held steady, with 1.774 million people still receiving benefits after filing their initial claim.

What’s the bottom line? The low level of Initial Jobless Claims suggests that employers are still trying to keep their workers. Yet, Continuing Claims are still trending near some of the hottest levels we’ve seen in recent years, as challenges remain for job seekers searching for their next position.

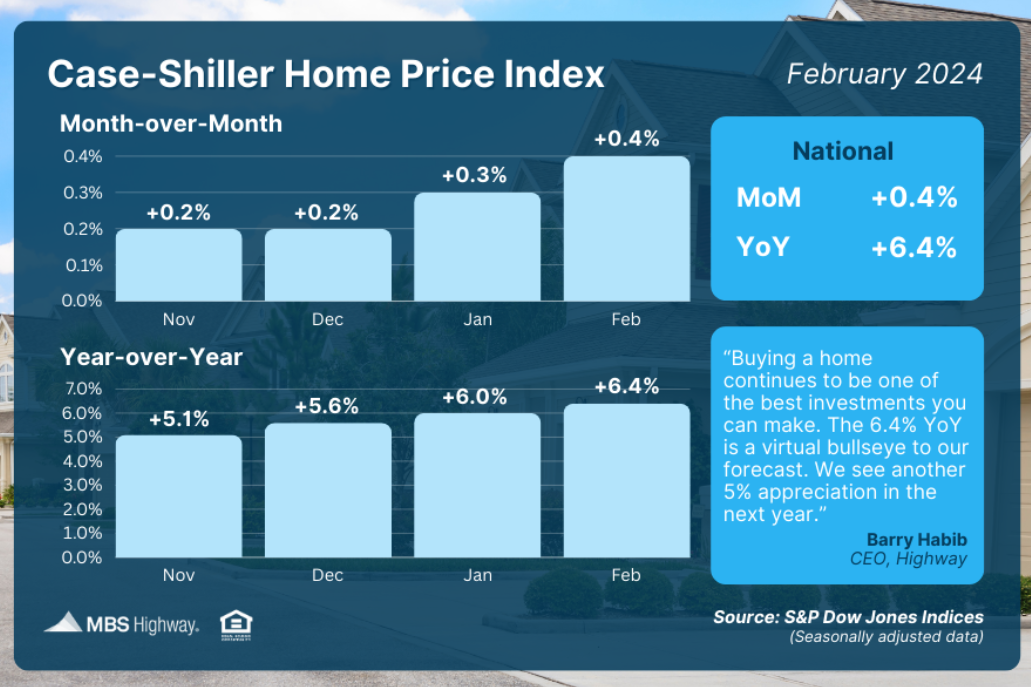

Home Price Gains Continue

The Case-Shiller Home Price Index, which is considered the “gold standard” for appreciation, showed home prices nationwide rose 0.4% from January to February after seasonal adjustment. Home values in February were also 6.4% higher than a year earlier, which is the fastest annual rate since November 2022. The Federal Housing Finance Agency’s (FHFA) House Price Index also reported a 1.2% jump in home prices from January to February, with prices 7% higher than the previous year. Note that FHFA does not include cash buyers or

jumbo loans, and these factors account for some of the differences in the two reports.

What’s the bottom line? S&P DJI’s Head of Commodities, Brian D. Luke, confirmed that national home prices are “at or near all-time highs” with all 20 cities in their composite index once again posting annual price increases. Home values are expected to remain supported this year, as buyer demand still outpaces tight supply. These indexes show that homeownership remains a fantastic opportunity for families to create wealth through appreciation gains.

Family Hack of the Week

It’s National Strawberry Month! This Strawberry Granola Parfait courtesy of Good Housekeeping makes for a delicious breakfast, snack or even dessert. Yields 1 parfait. In a 3-quart saucepan, cook 1 pound hulled strawberries, 3/4 cup sugar, 1/2 teaspoon cinnamon, and 1/2 teaspoon lemon peel on medium until strawberries are soft but still red, stirring, about 8 to 10 minutes. Transfer to a blender and puree until

smooth. Stir in 1/2 teaspoon vanilla and 1 tablespoon lemon juice. In an 8-ounce jar, add 1/2 cup granola, 1/2 cup yogurt, and the strawberry coulis in layers. Garnish with strawberries. Enjoy immediately or seal and refrigerate overnight for the next day.

What to Look for This Week

A much quieter week is ahead, but highlights include appreciation data from CoreLogic on Tuesday and the latest jobless claims on Thursday. Investors will also be closely watching Wednesday’s 10-year Note and Thursday’s 30-year Bond auctions for the level of demand.

Technical Picture

Mortgage Bonds rallied late last week, moving into a new trading range with a floor of support at their 200-day Moving Average and a ceiling at their 50-day Moving Average. The 10-year broke beneath its 25-day Moving Average and has more room for improvement until reaching the next floor at 4.418%.

If you have any questions, please contact me today.