Week of August 19, 2024 in Review

The Fed signaled rate cuts ahead while New Home Sales surprised to the upside. Here are the top stories:

- Powell Confirms, “The Time Has Come For Policy To Adjust.”

- Existing Home Sales Snaps Four-Month Losing Streak

- New Home Sales Surprise to the Upside in July

- Jobless Claims Sample Week

Powell Confirms “Time has come for policy to adjust.”

Fed Chair Jerome Powell spoke at the Jackson Hole Economic Symposium on Friday. His speech was definitely dovish as he confirmed a September 18 rate cut. Powell said, “the time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.”

While he was non-committal on the size of a cut, the market liked the confirmation that policy is changing and will begin to be less restrictive. Powell explained that inflation has declined significantly, and his confidence has grown that inflation is headed on a path to 2%. He also said that upside risks to inflation have

diminished, while downside risks to unemployment have increased. Clearly, the Fed is more concerned with the labor market versus inflation now.

On the labor market, Powell said that conditions are less tight than pre-pandemic when inflation was below 2%, meaning that the labor market would not be a source of inflation.

What’s the bottom line? The Fed Futures continues to price in a 100% change of a 25bp cut in September, with a 33% chance of 50bp. The market is putting a 73% chance of 100bp of cuts by year end, which would mean there has to be a 50bp cut at one of the next three meetings. The market is also pricing in another

125bp of cuts in 2025, which would be 225bp in total between this year and next and bring the Fed Funds rate down to 3.125%, which would still be above inflation.

Existing Home Sales Snaps Four-Month Losing Streak

Existing Home Sales, which measures closings on existing homes, rose 1.3% in July to an annualized pace of 3.95M units, which was in line with market estimates and broke a four-month losing streak. Sales were down 2.5% year over year.

This report likely measured people shopping for homes in May and June, when rates were above 7%. Rates have since come down, which we believe will lead to more sales in the upcoming reports. Inventory increased 0.8% month over month to 1.33M units. Inventory is now up 20% year-over-year, but it’s important to note that there is a seasonality to inventory and we always see inventory move up and peak around this time of the year, then begin to fall.

Based on the increased pace of sales, even with the increase in inventory, there is a four months’ supply of homes, which is down from 4.1 in the previous report and below a more normal market’s 4.6 months’ supply.

Homes remained on the market for 24 days on average, up from 22 days in June but this metric has been trending lower. In May, homes were on the market for an average of 24 days, less than the 26 days seen in April and 33 days in March. We also saw 24% of homes sold above the list price, down from 29% in the previous report but showing that there are still bidding wars in about a quarter of home sales nationwide.

The median home price was $422,600, down 1% from last month but up 4.2% from last year. First-time homebuyers accounted for 29% of sales, which was unchanged. Cash buyers accounted for 27% of sales, down from 28% in the previous report, while Investors made up 13%, down from 16%.

What’s the bottom line? The number of closings increased in July and some of the internals within the report point to demand remaining strong even in the face of elevated rates. Homes remained on the market for a short period, an average of 24 days in July.

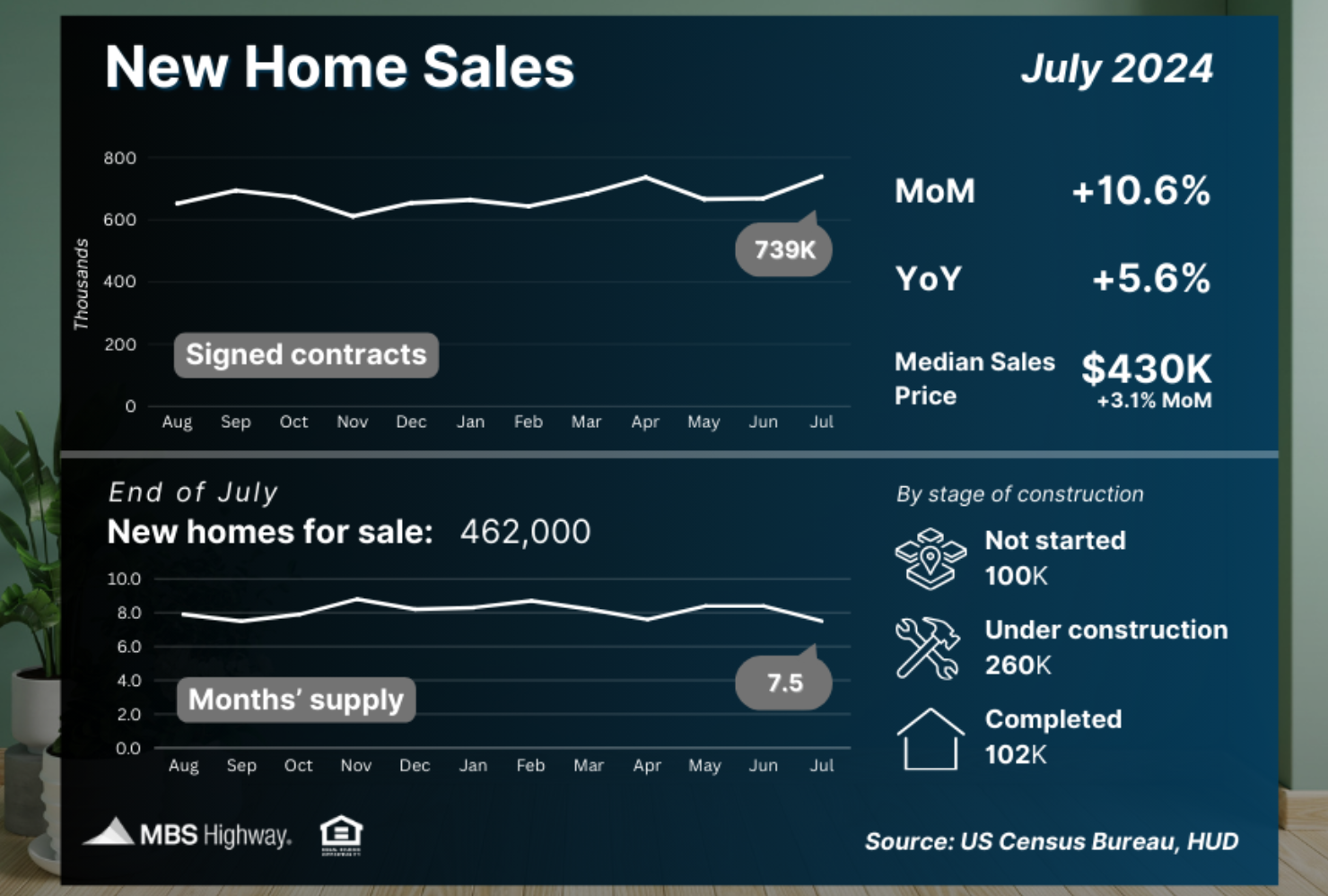

New Home Sales Surprise to the upside in July

New Home Sales, which measures signed contracts on new homes, rose 10.6% to a 739,000-unit annualized pace, blowing out estimates of a 1% rise. Additionally, June was revised significantly higher, causing July’s gain to appear lower. When considering the revision, sales rose 20% from the originally reported figure in June, which is very strong.

There were 462,000 new homes for sale at the end of July, which was down from a downwardly revised 467,000 in the previous report. At the current pace of sales, there is 7.5 month’s supply, which is down from 8.4. However, only 102,000 are completed, and when looking at the pace of sales versus homes that are

completed (available supply), there is only a 2.2 months’ supply, up from 2.1 in June.

This means that 360,000 homes are either not started or under construction, and it’s unclear how many will actually make it to the finish line as financing and carrying costs are very high. The median home price was reported at $429,800, which is up 3.1% from the previous month and down 1.4% from last year.

What’s the bottom line? Unlike the Existing Home Sales counterpart, which measures closings and likely represented buyers shopping in May and June, this shows people signing contracts in July and shows that demand is picking up as rates have moderated…And this report does not include the further rate drop we

have seen in August, which will likely lead to continued strength and acceleration in the sales figures.

Jobless Claims Sample Week

Initial Jobless Claims, which measures individuals filing for unemployment benefits for the first time, rose 4,000 to 232,000 but this figure is still lower than some of the readings last month. This applied some pressure to the Bond market, as it shows there are less firings happening but a lot of the other labor data are showing weakness. This week’s report encapsulates the sample week that the BLS uses in their Jobs Report modeling, and from this one component, it will likely help job growth figures.

Continuing Claims, which measures individuals continuing to receive benefits after their initial claim, rose 4,000 to 1.863M, still hovering near the highest level in almost three years. This metric continues to show that once someone is let go, it’s harder to get a job because of less hiring.

What’s the bottom line? Both Initial and Continuing Claims have trended higher this summer when compared to the start of the year, with Continuing Claims topping 1.8M each week since the start of June. This shows that the pace of layoffs over the last two months has picked up at the same time employers have

slowed down hiring.

Family Hack of the Week

August 31 is National Trail Mix Day, and this Pumpkin Seed Cherry Trail Mix courtesy of the Food Network makes for a healthy and delicious snack to enjoy. Yields about 6 cups.

- Preheat oven to 300 degrees Fahrenheit.

- Line 2 baking sheets with parchment paper.

- In a large bowl,

- toss 2 cups pumpkin seeds,

- 1 cup slivered almonds, and

- 3/4 cup raw sunflower seeds with 6 tablespoons pure Grade B maple syrup until evenly coated.

- Spread the nuts and seeds in a single even layer on the baking sheets and season with salt to taste.

- Bake for about 20 minutes until just golden, stirring several times with a spatula.

- Cool the nuts completely on the pan, then add 1 cup dried cherries and toss to combine.

- Store cooled trail mix in an airtight container at room temperature.

What to Look for This Week

Look for more housing news, starting with appreciation data for June from Case-Shiller and the Federal Housing Finance Agency on Tuesday. July’s Pending Home Sales will be reported on Thursday. Also on Thursday, we’ll see the second reading on second quarter GDP and the latest Jobless Claims. Friday brings the most crucial report of the week via the Fed’s favored inflation measure, Personal Consumption Expenditures.

Technical Picture

Mortgage Bonds have broken above a very important ceiling of resistance at 100.79. There is a lot of room for continued improvement before reaching the next ceiling at 101.18. The 10-year yield is testing an important floor at 3.80%. The last few times tested, this level has held, but a convincing break beneath it means that yields could go as low as 3.66%.

If you have any questions, please contact me today!