Week of October 21, 2024 in Review

September brought mixed news on home sales while unemployment filings suggest that employers have slowed down their pace of hiring. Read on for these stories and more:

- Existing Home Sales Slide for Second Straight Month

- New Home Sales Beat Estimates

- Continuing Jobless Claims Highest Since November 2021

- Latest LEI and Beige Book Suggest Slowing Economy

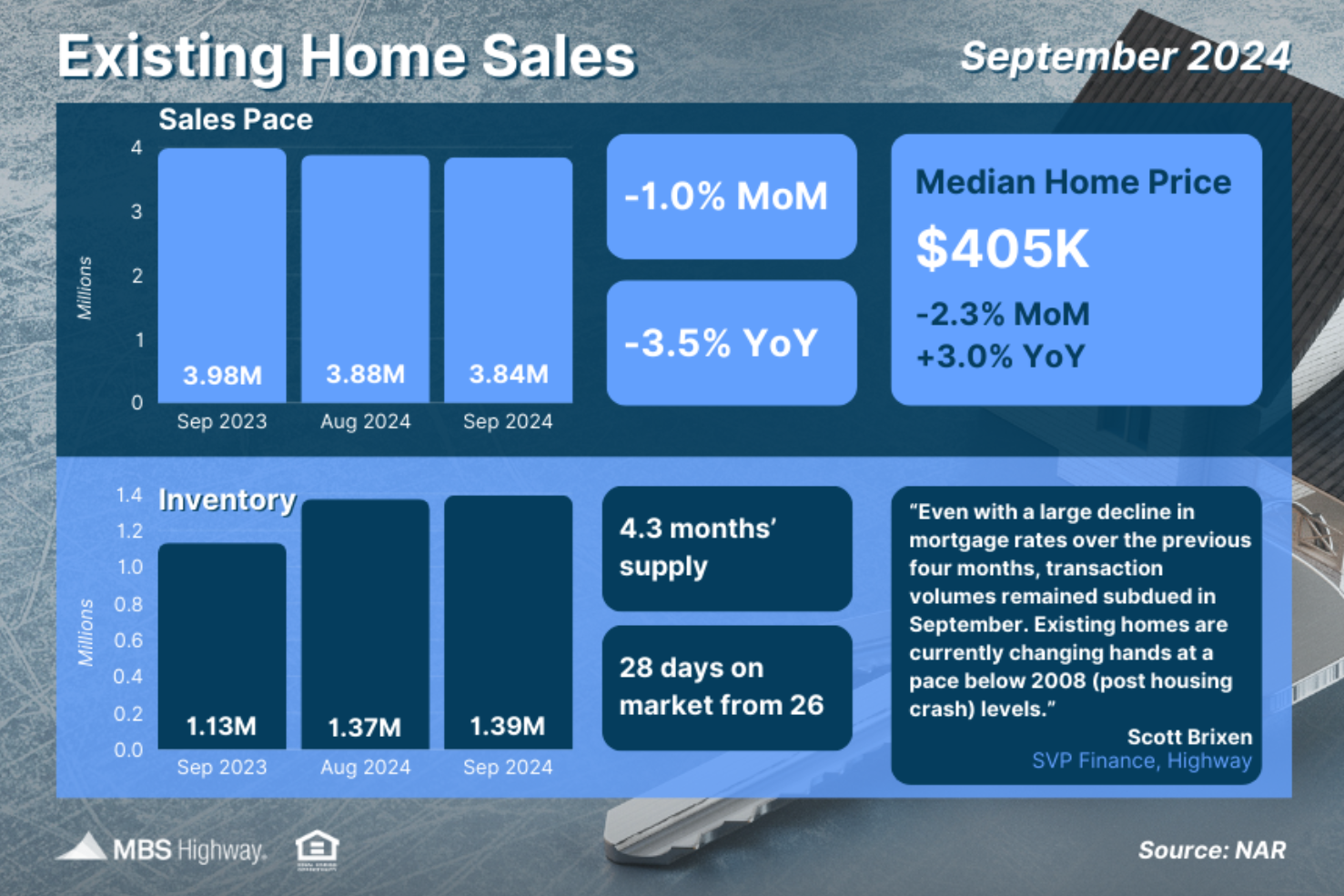

Existing Home Sales Slide for Second Straight Month

Existing Home Sales, which reflect closings on existing homes, fell for the second straight month in September, down 1% from August and 3.5% from a year ago. The 3.84-million-unit pace represents a 14-year low as NAR’s Chief Economist, Lawrence Yun, noted that “home sales have been essentially stuck at around a four-million-unit pace for the past 12 months.”

Regarding inventory, there were 1.39 million homes available for sale at the end of September, up 1.5% from August and 23% from a year earlier. While this sounds like a big jump, the rise is from very low numbers and inventory remains well below pre-pandemic levels.Plus, many homes counted in existing inventory are under contract and not truly available for purchase, meaning inventory is even tighter than the reporting implies. In fact, there were only 941,000 “active listings” at the end of last month.

What’s the bottom line? While the number of closings declined in September, some of the internals within the report point to buyer demand. Homes remained on the market for an average of 28 days in September, and while that’s an increase from 26 days in August, it’s still a relatively short period of time. In addition, 20% of homes sold above list price, showing that there are still bidding wars in about a fifth of sales nationwide. Plus, competition is expected to

rise when rates move lower.

All in all, the pent-up demand for homes combined with ongoing tight supply continues to bode well for housing as an investment and continued home price appreciation over time.

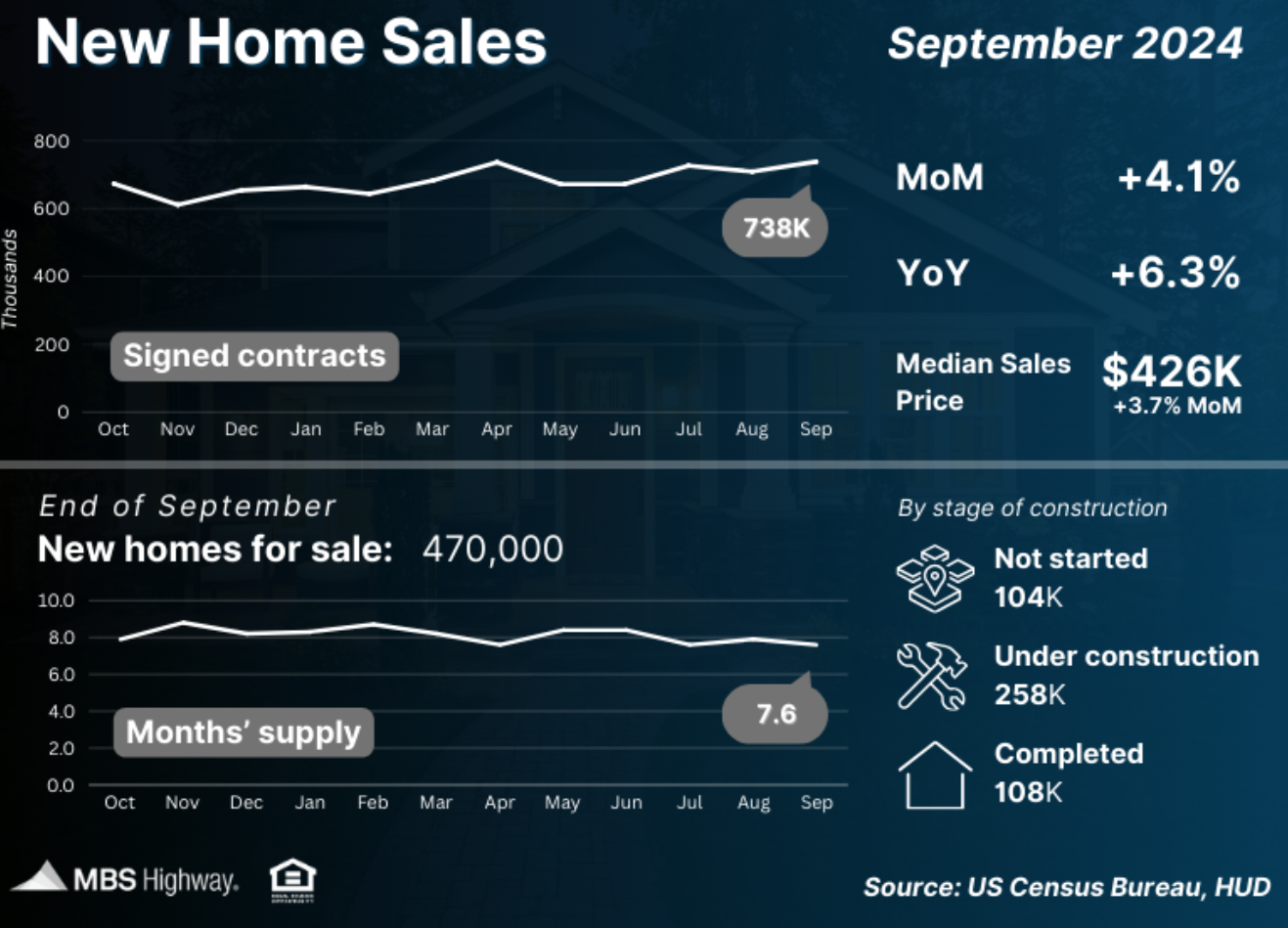

New Home Sales Beat Estimates

New Home Sales, which measure signed contracts on new homes, rose 4.1% from August to September, with the 738,000-unit pace reaching the highest level in over a year. Signed contracts were also 6.3% higher than they were in September of last year. There were 470,000 new homes for sale at the end of September, which was up slightly from 468,000 in August. However, only 108,000 were completed, with the rest either under construction or not even started yet, so more available supply is still needed.

What’s the bottom line? This latest report measures signed contracts in September, so it captured people shopping for homes when rates were lower than they are now. October’s New Home Sales report, which will be released on November 26, could show some weakness, given the recent move higher in rates.

Continuing Jobless Claims Highest Since November 2021

The number of people filing for unemployment benefits for the first time declined by 15,000 in the latest week, as 227,000 Initial Jobless Claims were reported. Continuing Claims rose by 28,000, with 1.897 million people still receiving benefits after filing their initial claim.

What’s the bottom line? Initial Jobless Claims declined after the recent spike in filings that were due in part to Hurricanes Helene and Milton. However, Continuing Claims remain elevated, as they have now topped 1.8 million for the last 20 weeks and just hit their highest level since November 2021. Employers have clearly slowed down their pace of hiring and people are collecting benefits for longer periods of time.

Latest LEI and Beige Book Suggest Slowing Economy

The Conference Board released their latest Leading Economic Index (LEI), which takes a broad look at the economy and tracks where it’s heading in the near term. September brought a 0.5% drop, which followed August’s 0.3% decline. This report has been negative for 29 out of the last 30 months, with the other month being flat.

What’s the bottom line? “Overall, the LEI continued to signal uncertainty for economic activity ahead and is consistent with The Conference Board expectation for moderate growth at the close of 2024 and into early 2025,” explained Justyna Zabinska-La Monica, Senior Manager, Business Cycle Indicators.

This correlates with the Fed’s latest Beige Book, which is a survey of economic conditions around the country. The report noted that, “On balance, economic activity was little changed in nearly all districts since early September, though two districts reported modest growth. Reports on consumer spending were mixed,

with some districts noting shifts in the composition of purchases, mostly toward less expensive alternatives.”

Family Hack of the Week

These Candy Bucket Cookies courtesy of the Food Network are a great way to enjoy leftover Halloween candy. Yields 20 cookies.

- Preheat oven to 325 degrees Fahrenheit.

- Line 2 baking sheets with parchment paper.

- In a large bowl, mix 2 cups plus 2 tablespoons all-purpose flour, 1/2 teaspoon baking soda and 1/2 teaspoon salt.

- In a separate bowl, combine 1 cup packed light brown sugar, 1 1/2 sticks salted butter (melted, then cooled slightly), 1/2 cup granulated sugar, 1 1/2 teaspoons vanilla, 1 large egg and 1 large egg yolk.

- Add in the dry ingredients and mix until just combined.

- Fold in 2 cups chopped leftover candy.

- Use an ice cream scoop to add dough to prepared baking sheets.

- Bake until slightly golden and puffy, around 14 to 17 minutes.

- Cool on a wire rack for 15 minutes, then enjoy.

What to Look for This Week

Housing, inflation and jobs data highlight a busy week of reports. Look for appreciation data on Tuesday, while Wednesday brings Pending Home Sales and the first estimate of third quarter GDP. The Fed’s favored inflation measure, Personal Consumption Expenditures, will be reported on Thursday.

We’ll also see updates on job openings Tuesday, private payrolls Wednesday, unemployment claims Thursday, and nonfarm payrolls and the unemployment rate Friday.

Technical Picture

Mortgage Bonds tested their 200-day Moving Average on Friday but were rejected lower. They ended last week just above support at 99.18. The 10-year also tested its 200-day Moving Average and moved higher. There is a lot of room for yields to rise before reaching the next ceiling at the 4.332% Fibonacci level.

If you have any questions, please contact me today!