Mortgage rates moved modestly lower this week, improving by .125% compared to last Monday, February 23rd. While that’s a welcome shift, the broader economic picture remains mixed.

Home prices continue to show resilience, inflation data surprised to the upside, and labor market signals remain complicated beneath the surface. Let’s break it down.

Mortgage Rates: Slight Improvement

The 30-year fixed rate improved week-over-week, supported by stable Treasury yields. Lower rates are gradually bringing buyers back into the market — but inflation remains the wild card influencing how much further rates can move.

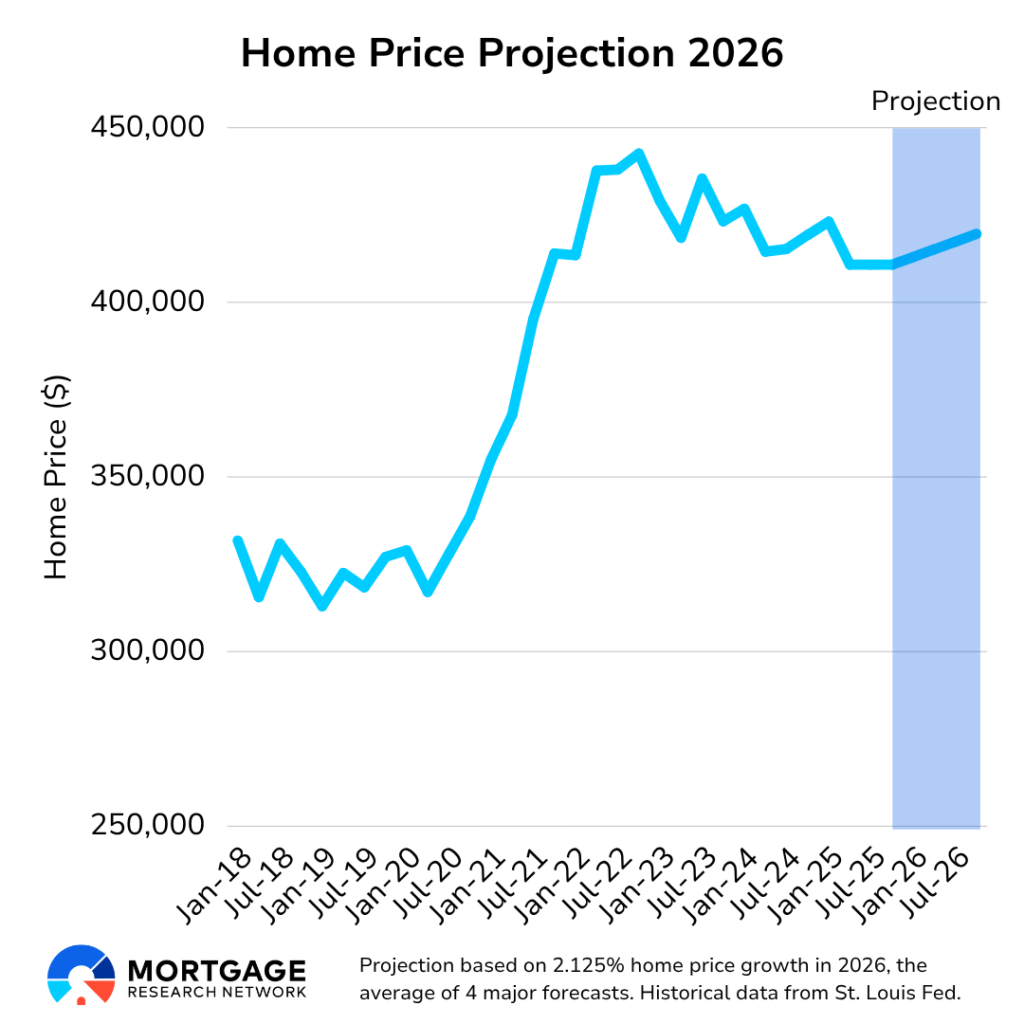

Home Prices Remain Supported by Demand & Limited Supply

Recent housing data shows stability, not weakness.

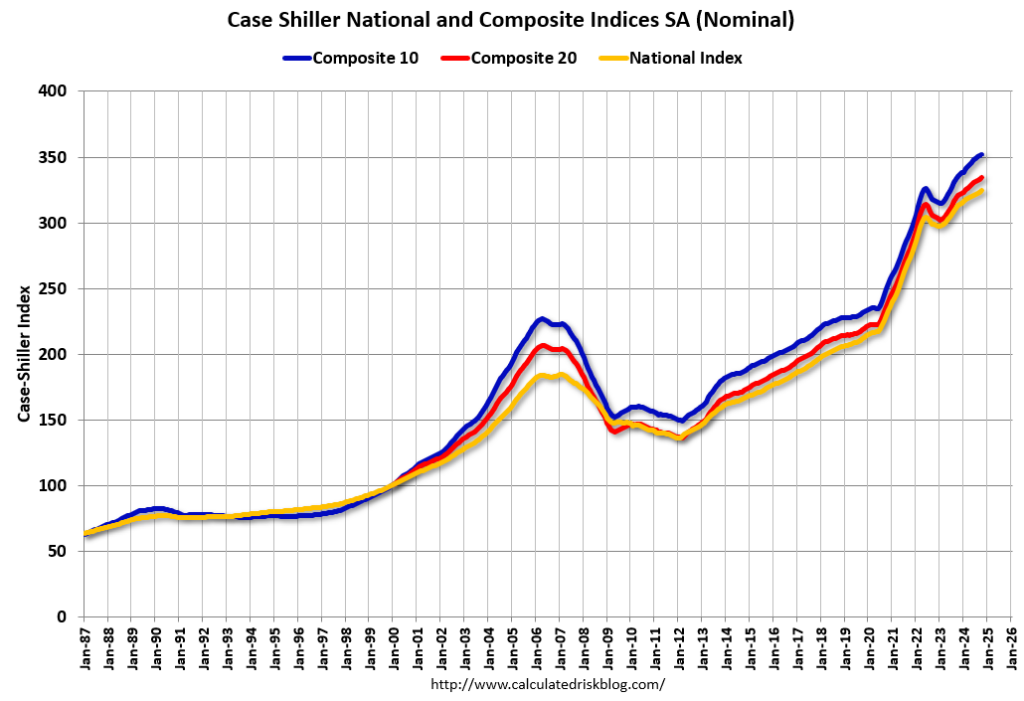

S&P CoreLogic Case-Shiller Index

- Prices dipped 0.3% (unadjusted) from November to December

- After seasonal adjustment, prices rose 0.4%

- National home prices are up 1.3% year-over-year

The Federal Housing Finance Agency House Price Index also showed:

- 0.1% monthly gain (seasonally adjusted)

- 1.8% annual growth

Lower mortgage rates are beginning to pull buyers back into the market, while limited housing inventory continues to prevent downward pressure on pricing.

Looking longer term, projections remain constructive. Fannie Mae and Pulsenomics forecast approximately 15% cumulative home price growth over five years — roughly a $75,000 increase on a $500,000 home.

If rates move meaningfully lower, renewed demand could accelerate price appreciation.

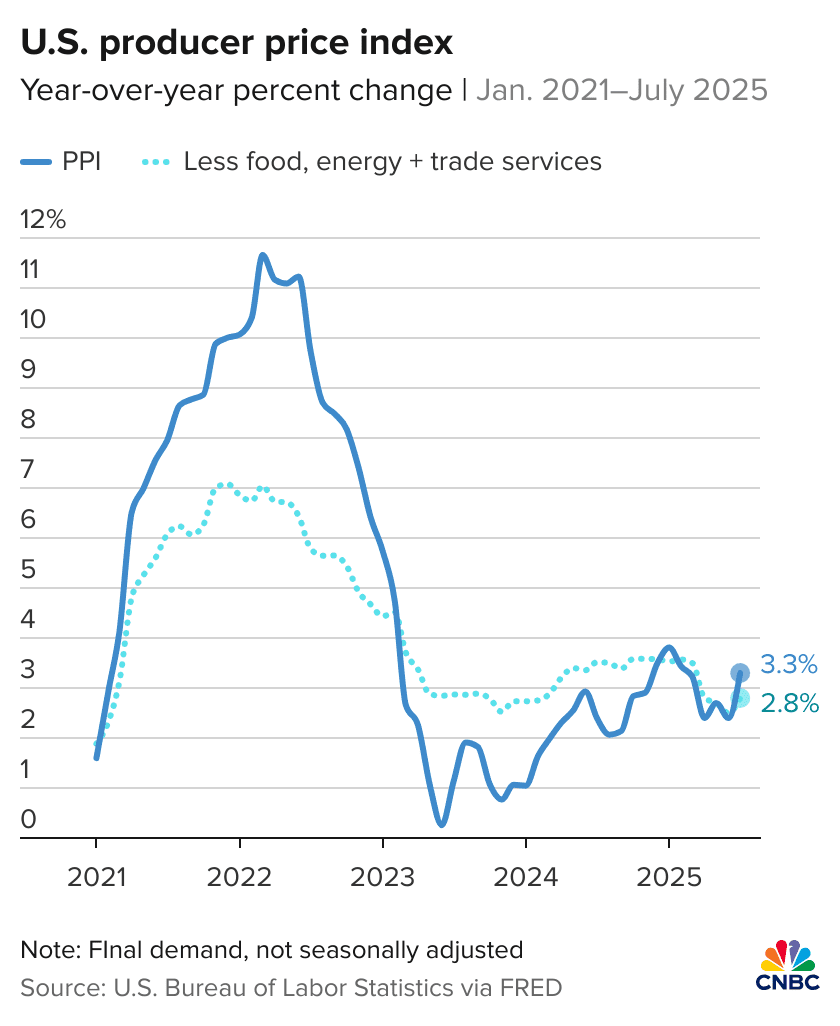

Wholesale Inflation Surprises to the Upside

Inflation remains the primary factor influencing Federal Reserve policy.

According to the Bureau of Labor Statistics:

- January Producer Price Index (PPI) rose 0.5% month-over-month

- PPI is up 2.9% year-over-year

- Core PPI increased 0.8% for the month

- Core PPI stands at 3.6% annually

Both headline and core readings came in above expectations.

Persistent wholesale inflation pressures may cause the Federal Reserve to remain cautious on rate cuts — even as parts of the labor market show signs of cooling.

This reduces the likelihood of aggressive near-term easing.

Labor Market: Stable on the Surface, Softer Underneath?

Labor data continues to send mixed signals:

- Initial jobless claims rose slightly to 212,000 (still historically low)

- Continuing claims declined to 1.833 million, though remain elevated

On the surface, layoffs remain low. However, growth in gig and contract work may be masking underlying strain. Many displaced workers are accepting temporary or 1099 project-based work while taking longer to secure full-time employment.

The labor market is not collapsing — but it is normalizing.

What’s Ahead This Week?

Markets will closely monitor key labor reports:

- Wednesday: ADP Private Payrolls

- Thursday: Weekly Jobless Claims

- Friday: Full Employment Report (Nonfarm Payrolls & Unemployment Rate)

These reports will help determine whether the recent rate improvement can continue — or whether inflation and labor resilience keep the Fed on hold.

Bottom Line

- Mortgage rates improved modestly this week.

- Home prices remain supported by demand and limited supply.

- Wholesale inflation remains elevated, keeping the Fed cautious.

- Labor data suggests stability, but with underlying complexity.

The market narrative remains balanced — not overheated, not collapsing.

As always, we’ll continue monitoring developments closely and provide updates as conditions evolve.